July Trading On NGSE Closes Mixed, Positive, As Many Stocks Remain Undervalued

Market Roundup for July

Trading activities on the Nigerian Stock Exchange for the month of July closed marginally higher on Wednesday as the Federal Government declared Thursday and Friday public holidays to celebrate the Muslim festival of Eid-El-Kabir.

During the month, the market resisted further decline after the profit taking activities witnessed in June, halting the bearish transition on mixed sentiments in the midst of improved buying interests, negative macroeconomic indices. All of these occurred in the midst of corporate earnings that are not as terrible as predicted due to the lockdowns occasioned by the Coronavirus (COVID-19) pandemic with telling effects on many economies across the globe, despite the disappointing numbers and some surprising numbers that reveals huge opportunities in the equity space.

The power of earnings and the momentum of the reporting season cannot be overemphasized, being factors that have helped the market indicator the period under review, regardless of the negative impact of the lockdown on the earnings power of companies. These corporate earnings are expected to reshape the market in the month of August and support recovery.

The government and Central Bank of Nigeria (CBN) intervention funds and stimulus packages are yet to start reflecting on economic fundamentals and indicators such as the Purchasing Managers’ Index (PMI) which is still below 50 points for three consecutive months. For the month of July, PMI read 44.9 points despite inching up from 44.1point in June, while Consumer Price Index rose to 12.56% in the month of June, from May position of 12.40%, while unemployment rate continued its northward growth at 68% in the aftermath of the pandemic outbreak.

We believe that a change in fiscal policy stance, structural adjustments, early disbursement of capital project funds and real change in implementation style of the government will further hasten economic recovery, by enhancing productivity and national output needed to support growth.

The mixed trend during the period under review was obvious in the 21 trading sessions of the month during which the market closed negative for 12 days, and positive in nine to stop the previous month’s negative stance. It also reduced the year-to-date loss suffered by the NSE’s All-Share Index to 8%, owing to low price attraction and effects of the earnings season. Despite other challenges, many equities remained undervalued, offering high margins of safety and upside potentials.

Meanwhile, during the month under review, the benchmark NSEASI gained 214.57 basis points, closing at 24,693.73bps, after touching a high of 24,783.61bps and low of 23,961.14bps, from the 24,479.16bps it opened for the month, representing a 0.88% rise. This came with a strong buy-market position that impacted prices of high cap stocks, thereby resisting decline within the month.

The buying volume of total transactions for the month was 89%, while selling position was 11%, while volume index for the period was 0.65.

Market capitalisation for the month gained N110bn, closing at N12.88tr, from an opening value of N12.77tr, representing a 0.86% appreciation in value.

The market sustained a mixed sentiment and trend for stocks, especially with the earnings reporting season on the expected impact of the CBN intervention funds, 2020 capital budget implementation to help improve liquidity. Crude oil prices remained relatively stable at above $40 per barrel in the midst of a weakening US$ and depreciation of the Naira against other currencies.

Traded volume for the month was down by 12.29% to 4.21bn, shares from 4.8bn units in the preceding month, even as market breadth for the month was negative with decliners outnumbering advancers in the ratio of 71:23. This was despite the fact that the benchmark index closed marginally up in the period under consideration.

The sectoral performance chart below shows that the NSE Industrial Goods and Premium indices drove the market the most in the month under review. While the industrial Goods index gained 3.88%, the NSE Premium index followed with 3.79%, outperforming the NSEASI in the period.

Other sectoral indexes closed lower during the month, led by the NSE Oil/Gas which lost 13.3%, followed by the NSE Consumer Goods that shed 8.88%; the NSE Insurance, 5.69%; NSE Pension, 2.41%; and NSE Banking, 1.19%.

The month’s best performing stocks were Ikeja Hotel, which rallied on market forces, despite the negative sentiment for stocks in the hospitality sector, closing 17.89% above its opening price; followed by Unity Bank, which appreciated by 15.09%; while energy company, Ardova chalked of 14.47%; and United Capital, 12.11%.

Among the month’s top gainers during the month are: Dangote Cement, 10.78%; Redstar Express, 8.98%; Lafarge Africa, 8.80%; Vitafoam, 8.49%; Okomu Oil Palm, 6.46%; and Airtel Africa, 5.87%; among others.

Best Performing Stocks in July 2020

Securities Sector Open Close % Change Remarks

Ikeja Hotel Services 0.95 1.12 17.89 Market forces

Unity Bank Banking 0.53 0.61 15.09 Market forces

Ardova Oil/Gas 11.75 13.45 14.47 Sentiment

Ucap Other Financials 2.56 2.87 12.11 Improved EPS

Dangote Cement Industrial Goods 128.00 141.80 10.78 Low Priced Attraction

Redstar Express Services 3.23 3.52 8.98 Div Expectation

Wapco Industrial goods 10.80 11.75 8.80 Improving EPS

Vatifoam Consumer goods 5.30 5.75 8.49 Strong EPS

Okomu Oil Agro-Business 70.40 74.95 6.46 Strong EPS

Airtel Africa Telecoms 328.70 348.00 5.87 Sentiment

Source; Investdata Research

The worst performing stocks included Arbico, which lost 26.46%, linked to its unimpressive numbers and negative impact of the pandemic on the sector; Julius Berger lost 24.43% as a result of its weak performance; just as Learn Africa declined by 21.71%; followed by Unilever Nigeria, 19.93%; and Seplat, 19.64% on the back of negative and declining earnings performance.

Worst Performing Stocks in July 2020

Securities Sector Open Close % Change Remarks

Arbico Housing 1.89 1.39 -26.46 Poor Performance

Julius Berger Construction 19.85 15.00 -24.43 Weak Performance

Learn Africa Services 1.29 1.01 -21.71 Market Forces

Unilever Consumer goods 16.30 12.15 -19.93 Worsen weak numbers

Seplat Oil/Gas 386.00 310.20 -19.64 Impact low oil price

Conoil Oil/Gas 21.00 16.90 -19.52 Price adjustment for Div

International Brew Consumer goods 4.10 3.30 -19.51 Negative Account for 3yrs

Berger Paints Industrial goods 7.45 6.05 -18.75 Market forces & weak EPS

Nahco Services 2.45 2.00 -18.37 Market forces

Uacn Property Housing 0.99 0.81 -18.18 Red Accounts

Source: Investdata Research

Technical Analysis of July market

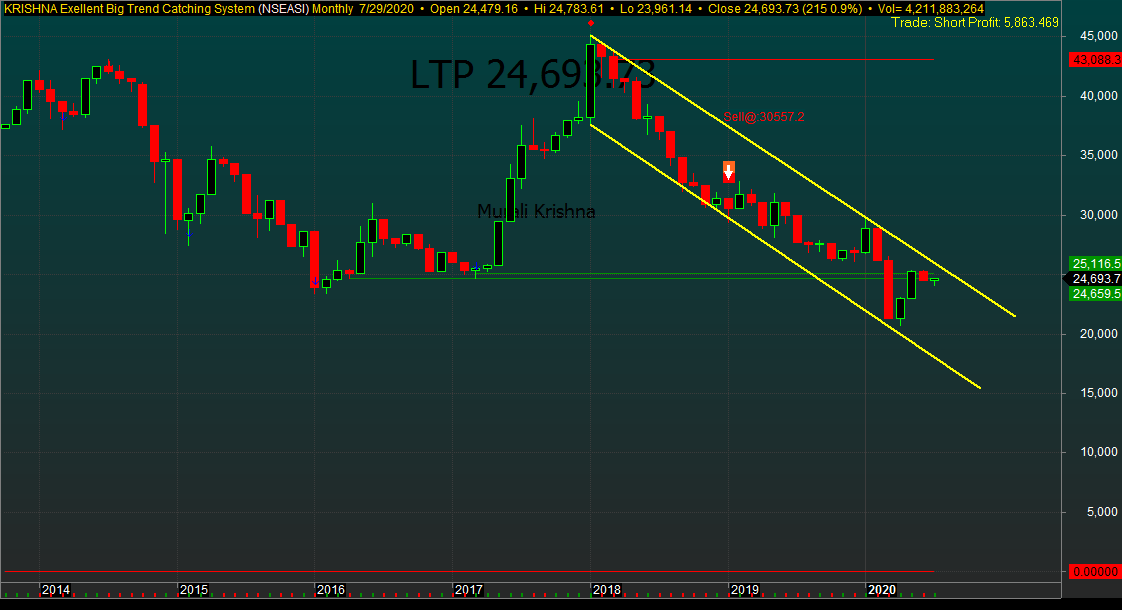

NSEASI MONTHLY TIME FRAME

The NSEASI’s monthly chart above has remained well below the 20 and 50-Day Moving Averages since December 2019 on a bearish channel, despite various attempts at a rebound, especially from the March 2020 dip that created wealth for smart traders and discerning investors. The market is resisting further decline as revealed by the chart which supports an uptrend after the earnings season. The mixed sentiment is likely to continue driving sectoral rotation on the strength of the numbers released.

Where To Invest And Expectations For August & September

The global economy remains unstable and depressed in the aftermath of the virus outbreak as the debt profile of many nations are on the rise, while economies try to rebound, amidst fear of a second wave of the Covid-19 pandemic and the geopolitical crisis threatening the recovery. In Europe and the U.S, the near-term growth outlook remains unpredictable, as political and economic uncertainties threaten the moderate recovery despite the news of vaccine discovery.

Back home, despite the negative macroeconomic data, the expected impact of the government and CBN bailout funds to support economic recovery in this quarter and beyond has started on a positive note to trigger confidence among equity market players. This is considering the low interest rate environment and inflation, coupled with mixed half-year earnings reports which offer insights into how the full-year outings would play out in terms of payout and earnings performance capable of driving or supporting future prices.

In August, we expect inflation figure for the month of July to be released by the National Bureau of Statistics (NBS) and the continued rally resulting from a combination of factors. These include the Naira devaluation, high cost of transporting goods and persons, as well as the heightening insecurity, among others, just as the PMI could improve slightly, supporting the seeming recovery. Nigeria’s manufacturing sector’s Q2 numbers were mixed, reflecting the impact of the pandemic on the sector and the economy at large.

The May year-end accounts and the remaining quarterly earnings are expected in this month, a situation that is likely to impact the market as other interim dividend paying stocks announce their results in August. Also, as investors and analysts interpret the recent scorecards to reposition and balance their portfolios ahead of Q3, this will keep the market oscillating in the period. The recent Q2 numbers are in line with market expectations, but surprises came out from different companies and sectors, a situation likely to strengthen market fundamentals as businesses continue to find direction.

The low valuation in the market was despite the April rebound, as many stocks remain undervalued given their intrinsic values, which should guide investors and help them know where to look in their search for profitable equity investors for the rest of the year while protecting their capital.

Traders and investors who understand the importance of combining fundaments and technical analysis in making investment decisions in the stock market should take this opportunity of numbers released so far to reshape the market while positioning for short, medium and long term gains. This is especially as candlestick formation at the end of July signal uptrend. Other sectors to consider for investment are banking, agribusiness, building material, telecoms and insurance after carefully study of the recent price pattern and fundamental data available in the market.

What to expect in August and September

Release of the May full-year earnings, since August is the end of the statutory 90-day period for audited results. This numbers from blue-chip companies may strengthen market fundamentals, if positive.

The oscillating trend of equity prices as a result of repositioning of portfolio along the line of positive numbers and profit taking.

Market outlook for the new month remains mixed as more quarterly and full-year earnings are expected. But with the mixed sentiment and momentum, the market is expected to extend it volatility, even as economic recovery may strengthen market fundamentals, if the 2020 capital budget is implemented judiciously.

The relative low Price-to-Earnings in market may further attract demand for stocks, but invest wisely, using bids, offers and volume when taking decisions as a trader.

Managing risk and protecting capital at this point is very important, so you will be able to determine when to buy or sell, by watching the stocks and the market, using technical analysis and watch list to buy right.

Let numbers released by companies guide your decision and time to stay in any particular position.

To learn how to manage trading risk, get INVESTDATA comprehensive stock market trading and investing home study pack where short trading strategies and how to identify quality companies to invest before the market look toward ii were discuss.

NB:The home study packs and videos that will help you prepare and take advantage of the current happening in the market and economy are available at Investdata. How to invest or trade profitably in changing market dynamics and recession. Mastering earnings season for profitable investment To obtain your pack send ‘Yes’ or ‘Stock’ to 08028164085,08032055467, 08111811223 now.

Ambrose Omordion

CRO|Investdata Consulting Ltd

info@investdataonline.com

info@investdata.com.ng

amberose.o@investdataonline.com

ambroseconsultants@yahoo.com

Tel: 08028164085, 08032055467

https://investdata.com.ng/july-trading-on-ngse-closes-mixed-positive-as-many-stocks-remain-undervalued/

Comments

Post a Comment