CCNN: Enhanced Production Capacity, Improved Valuation Post-Merger

Company: Cement Company of Northern Nigeria (CCNN)

Rating: Buy

Market Price at Earnings Release: N25.30

Current Market Price: N18.45

Highest Price 52wks: N32.00

Lowest Price 52wks: N10.42

Intrinsic Value: N45.27

Previous Production Capacity: 500,000mt/annum

Additional Production Capacity from Merger: 1.5m MT/annum

By: Jeariogbe Tunde Segun (Equity Analyst)

Rating: Buy

Market Price at Earnings Release: N25.30

Current Market Price: N18.45

Highest Price 52wks: N32.00

Lowest Price 52wks: N10.42

Intrinsic Value: N45.27

Previous Production Capacity: 500,000mt/annum

Additional Production Capacity from Merger: 1.5m MT/annum

By: Jeariogbe Tunde Segun (Equity Analyst)

Key Financial Tickers

• This report treats the nine-month financial performance of CCNN for the period ended 30th September, 2018, compares same with figures released in the similar period of 2017. And then, observes various new developments in the company to predict expectations in subsequent financial reports.

• Please understand that the share outstanding used in this analysis is 1,256,677,766 ordinary shares and not 13,143,500,966 units. This is because the result was released before the newly listed shares that increased the share outstanding of CCNN in December, 2018

• One key development in the cement company is its merger with Kalambaina Cement Company Limited, a wholly owned subsidiary of BUA Cement Limited, incorporated in Nigeria.

• Before now, CCNN operated as a 500,000 metric tons per annum company and the merger brings in an additional 1.5m metric tons per annum, increasing CCNN’s capacity to 2m metric tons per annum.

• As noted above, the merger accommodated the shareholders of Kalambaina Cement Company and so, had increased CCNN’s share outstanding to 13,143,500,966 from the previous 1,256,677,766 units

• Recall that BUA is one major shareholder of CCNN before now. In other words, since Kalambaina is wholly owned by BUA, one can conclude that it has increase its stake in CCNN

The Company’s Product/Strength

• A major strength of CCNN is its Strong presence in the North Western space. If it continues to consolidate on its near monopolistic advantage in Nigeria’s North West geo-political zone, without playing for size with its bigger competitors, then its revenue is sustainable.

• Please understand that its supposed major competitor in the northern part of the country is now a major part owner of the business. This is an added advantage to its domination of the area

• Considering the increase the merger brought into the share outstanding of CCNN and the growth in production capacity, it will be necessary to observe at least two consecutive earnings from the company post-merger, to arrive at conclusive growth expectation from the company.

• In other words, the state of Kalambaina in terms of facilities and customer base will need to be established, going forward, for better projection.

• This report treats the nine-month financial performance of CCNN for the period ended 30th September, 2018, compares same with figures released in the similar period of 2017. And then, observes various new developments in the company to predict expectations in subsequent financial reports.

• Please understand that the share outstanding used in this analysis is 1,256,677,766 ordinary shares and not 13,143,500,966 units. This is because the result was released before the newly listed shares that increased the share outstanding of CCNN in December, 2018

• One key development in the cement company is its merger with Kalambaina Cement Company Limited, a wholly owned subsidiary of BUA Cement Limited, incorporated in Nigeria.

• Before now, CCNN operated as a 500,000 metric tons per annum company and the merger brings in an additional 1.5m metric tons per annum, increasing CCNN’s capacity to 2m metric tons per annum.

• As noted above, the merger accommodated the shareholders of Kalambaina Cement Company and so, had increased CCNN’s share outstanding to 13,143,500,966 from the previous 1,256,677,766 units

• Recall that BUA is one major shareholder of CCNN before now. In other words, since Kalambaina is wholly owned by BUA, one can conclude that it has increase its stake in CCNN

The Company’s Product/Strength

• A major strength of CCNN is its Strong presence in the North Western space. If it continues to consolidate on its near monopolistic advantage in Nigeria’s North West geo-political zone, without playing for size with its bigger competitors, then its revenue is sustainable.

• Please understand that its supposed major competitor in the northern part of the country is now a major part owner of the business. This is an added advantage to its domination of the area

• Considering the increase the merger brought into the share outstanding of CCNN and the growth in production capacity, it will be necessary to observe at least two consecutive earnings from the company post-merger, to arrive at conclusive growth expectation from the company.

• In other words, the state of Kalambaina in terms of facilities and customer base will need to be established, going forward, for better projection.

Corporate Figures

• Turnover (TO) reported for the first nine months of 2018 is 43.61% above that of the corresponding quarter in 2017. A total of N19.57 billion was posted for the period, as against the N13.62 billion reported in Q3-2017.

• Selling and distribution expense was 47.87% above what was reported in 2017. The index moved from N652.74 million to N965.21 million.

• Similarly, Administrative Expensive posted for the period increased to N1.924 billion from N1.648 billion.

• Thus, Operating Profit soared above the 2017 figure, having grown to N5.757 billion from the previous N2.970 billion posted in Q3-2017

• Profit before Tax was estimated at N5.728 billion, compared to the N2.857 billion reported for same period in 2017.

• Having considered Tax Expenses for the period, N4.10 billion was reported as the Profit for the period, this is 96.94% above corresponding quarter’s profit of N2.03billion.

• Retained earnings improved over the corresponding period by 40.36%, moving from N8.98 billion to N12.61 billion.

• Non Current Assets stood at 26.59% above what was reported in the previous quarter of 2017. In the report under analysis, it was estimated at N14.53 billion as against N11.42 billion in 2017

• Meanwhile, Current Assets improved by 44.69% from the previously reported N11.06 billion to N16.00 billion

• Non Current Liabilities on the other hand grew by 3.56% as it is currently estimated at N2.82 billion compare to the N2.73 billion posted in third quarter of 2017

• Current Liabilities is currently valued at N10.86 billion, this is 51.86% above the N9.01 billion reported in 2017.

• See the table below for details.

• Turnover (TO) reported for the first nine months of 2018 is 43.61% above that of the corresponding quarter in 2017. A total of N19.57 billion was posted for the period, as against the N13.62 billion reported in Q3-2017.

• Selling and distribution expense was 47.87% above what was reported in 2017. The index moved from N652.74 million to N965.21 million.

• Similarly, Administrative Expensive posted for the period increased to N1.924 billion from N1.648 billion.

• Thus, Operating Profit soared above the 2017 figure, having grown to N5.757 billion from the previous N2.970 billion posted in Q3-2017

• Profit before Tax was estimated at N5.728 billion, compared to the N2.857 billion reported for same period in 2017.

• Having considered Tax Expenses for the period, N4.10 billion was reported as the Profit for the period, this is 96.94% above corresponding quarter’s profit of N2.03billion.

• Retained earnings improved over the corresponding period by 40.36%, moving from N8.98 billion to N12.61 billion.

• Non Current Assets stood at 26.59% above what was reported in the previous quarter of 2017. In the report under analysis, it was estimated at N14.53 billion as against N11.42 billion in 2017

• Meanwhile, Current Assets improved by 44.69% from the previously reported N11.06 billion to N16.00 billion

• Non Current Liabilities on the other hand grew by 3.56% as it is currently estimated at N2.82 billion compare to the N2.73 billion posted in third quarter of 2017

• Current Liabilities is currently valued at N10.86 billion, this is 51.86% above the N9.01 billion reported in 2017.

• See the table below for details.

Liquidity/Risk Ratios

• Current Ratio stood above unity, implying the company’s ability to settle current liabilities as at when due.

• The beta value which measures equity volatility on the exchange stood above market beta, but below industry average. Signifying appreciable volatility/patronage.

• Interest coverage is far below the industry average, estimated at 106.59x implying the ability to take care of interest due on its interest yielding liabilities.

• Current Ratio stood above unity, implying the company’s ability to settle current liabilities as at when due.

• The beta value which measures equity volatility on the exchange stood above market beta, but below industry average. Signifying appreciable volatility/patronage.

• Interest coverage is far below the industry average, estimated at 106.59x implying the ability to take care of interest due on its interest yielding liabilities.

Profitability Ratios

• Cost of Sales Margin is currently estimated at 55.91%, slightly below the 61.65% estimated last year.

• Profit Before Tax margin is 29.27%, which is also above the 20.97% margin estimated from the corresponding quarter figures

• Similarly, Profit After Tax margin stood above that of Q1-2017. We have currently estimated 20.49% as against the previous 14.94%.

• Return on Average equity is currently estimated at 23.80% this is 58.12% above the 15.05% achieved in similar period of 2017.

• Return achieved on Average Assets is now 13.13%, as against 9.03%.

• Cost of Sales Margin is currently estimated at 55.91%, slightly below the 61.65% estimated last year.

• Profit Before Tax margin is 29.27%, which is also above the 20.97% margin estimated from the corresponding quarter figures

• Similarly, Profit After Tax margin stood above that of Q1-2017. We have currently estimated 20.49% as against the previous 14.94%.

• Return on Average equity is currently estimated at 23.80% this is 58.12% above the 15.05% achieved in similar period of 2017.

• Return achieved on Average Assets is now 13.13%, as against 9.03%.

Efficiency Ratios

• Testing the management efficiency, when the Asset Turnover was gauged, the Ratio improved by marginal 6.01% from 60.45% to 64.08%.

• Also tested was the Equity Turnover, which currently stands at 116.14%, as against the 100.73% estimated in 2017.

• In other words, the equity was multiplied 1.81x through the first nine months of 2018 financial activities, slightly above the 1.67x in Q3-2017.

• It was also estimated that Fixed Assets turnover is same as 64.08% above the 60.45% estimated in Q3-2017.

• Testing the management efficiency, when the Asset Turnover was gauged, the Ratio improved by marginal 6.01% from 60.45% to 64.08%.

• Also tested was the Equity Turnover, which currently stands at 116.14%, as against the 100.73% estimated in 2017.

• In other words, the equity was multiplied 1.81x through the first nine months of 2018 financial activities, slightly above the 1.67x in Q3-2017.

• It was also estimated that Fixed Assets turnover is same as 64.08% above the 60.45% estimated in Q3-2017.

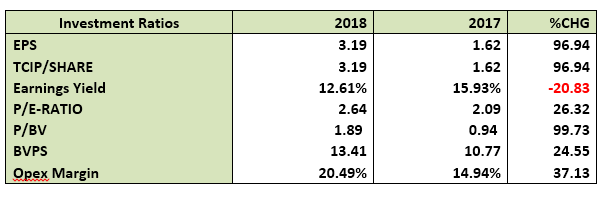

Investment Ratios

• Following same trend as in the earnings, the amount earned per unit of CCNN in its Q3- financial performance (EPS) improved by 96.94% against the comparable period of 2017. The current EPS estimate is N3.19.

• Price Earnings Ratio (PE/Ratio) is currently estimated at 2.64x as against the previous 2.09x. Although this is mainly used in confirming investment recouping time, it is also indicative of investor sentiments on the price of CCNN.

• As we speak the book value of CCNN is currently N13.41 above the N10.77 in 2017. When this is placed side by side the current market price (N18.45), one might declare an overpriced position.

• Following same trend as in the earnings, the amount earned per unit of CCNN in its Q3- financial performance (EPS) improved by 96.94% against the comparable period of 2017. The current EPS estimate is N3.19.

• Price Earnings Ratio (PE/Ratio) is currently estimated at 2.64x as against the previous 2.09x. Although this is mainly used in confirming investment recouping time, it is also indicative of investor sentiments on the price of CCNN.

• As we speak the book value of CCNN is currently N13.41 above the N10.77 in 2017. When this is placed side by side the current market price (N18.45), one might declare an overpriced position.

Valuation

We have valued each units of CCNN share price out assuming an improve performance from the first quarter of 2019. It should be noted that the new shares was listed on the 31st December, 2018, implying that the full utilisation of the merger will commence from the first quarter of 2019. As noted above, certain fundamentals could not be fully established by the time this report was compiled. Such fundamentals include: The financial health of Kalabaina Cement, the state of machineries, staff quality along with the customer base. Making these factors more relevant is the incoming shareholders from Kalambaina which already increased the share outstanding by over 1000%. Nevertheless, it should also be noted that the merger brings in an outstanding improvement to CCNN production capacity.

Considering the above, we up our valuation for each unit of CCNN shares from the previous N25.17 to N45.27.

We have valued each units of CCNN share price out assuming an improve performance from the first quarter of 2019. It should be noted that the new shares was listed on the 31st December, 2018, implying that the full utilisation of the merger will commence from the first quarter of 2019. As noted above, certain fundamentals could not be fully established by the time this report was compiled. Such fundamentals include: The financial health of Kalabaina Cement, the state of machineries, staff quality along with the customer base. Making these factors more relevant is the incoming shareholders from Kalambaina which already increased the share outstanding by over 1000%. Nevertheless, it should also be noted that the merger brings in an outstanding improvement to CCNN production capacity.

Considering the above, we up our valuation for each unit of CCNN shares from the previous N25.17 to N45.27.

Comments

Post a Comment